The narrative around Latin American altcoin adoption has always carried a Bitcoin-centric framing. The region discovers crypto, the region buys Bitcoin, Bitcoin protects savings from inflation. It was a clean story, and for a period it was largely accurate. In 2025, the data has moved decisively past it.

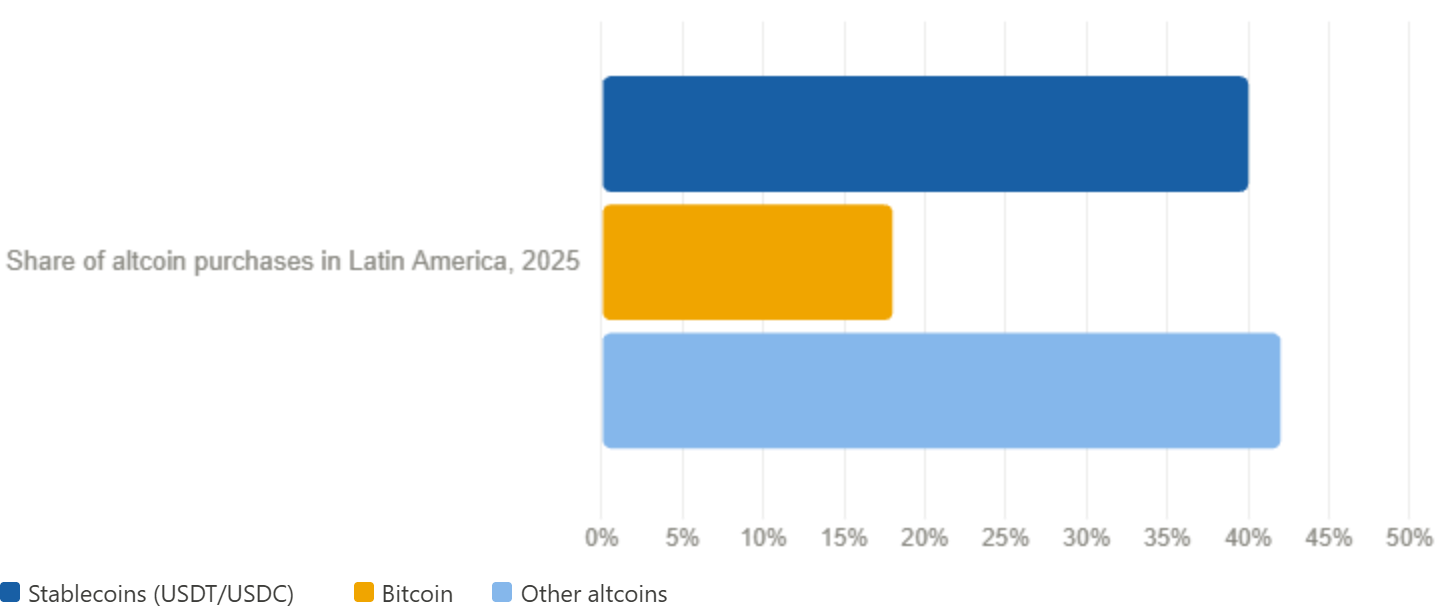

Stablecoins now account for 40% of all altcoin purchases across Latin America. Bitcoin accounts for 18%. The asset that the Western altcoin community still treats as the default entry point for new adopters — the obvious first purchase, the gateway asset, the thing you buy when you decide to get into crypto — is being outpurchased by dollar-pegged tokens at more than two to one in one of the world’s most important emerging market altcoin economies.

That gap isn’t a temporary anomaly. It’s the product of a specific and durable set of economic conditions that aren’t going away — and it’s reshaping what altcoin adoption actually means in a region of 650 million people.

The Numbers That Reframe the Whole Conversation

The allocation gap between stablecoins and Bitcoin in Latin America tells a story about what people actually need from the altcoin ecosystem when financial survival is the primary motivation — as opposed to what they want when portfolio optimization is. Western altcoin discourse is dominated by the latter framing. Latin American adoption is driven almost entirely by the former.

When a Venezuelan bolivar loses purchasing power faster than a savings account can accumulate interest, the relevant question isn’t whether Bitcoin will outperform equities over the next decade. It’s whether your savings will be worth something next month. When an Argentine peso depreciates faster than wages can compensate, the hedge you need isn’t volatile — it’s stable. The name stablecoin isn’t marketing language for the populations driving these numbers. It’s a literal description of the property they’re paying for.

Three Forces Driving the Stablecoin Preference

The data points to three distinct but reinforcing drivers behind Latin America’s stablecoin preference, and understanding each separately matters because they affect different populations in different ways.

Inflation and currency depreciation is the most obvious and most discussed driver. Argentina, Venezuela, and to varying degrees Brazil, Colombia, and several Central American economies have experienced sustained currency weakness that makes holding local fiat a losing proposition for anyone with savings to protect. The traditional alternative — buying US dollars — requires either access to formal currency markets that impose restrictions and unfavorable official rates, or participation in informal parallel markets that carry legal risk and physical security concerns.

USDT and USDC offer a third path: dollar-denominated value held in a digital wallet, accessible without a US bank account, transferable without going through official currency channels, and protected from the local inflation rate with the same effectiveness as physical dollar holdings. For the populations experiencing the sharpest currency depreciation, stablecoins aren’t an altcoin product. They’re a dollarization mechanism — and they’re more accessible than any other dollarization mechanism that has previously existed.

Weak banking infrastructure is the second driver, and it affects a different slice of the population than the inflation hedge use case. Latin America has significant unbanked and underbanked populations — people without formal bank accounts, without credit histories, without access to the financial products that allow participation in the modern economy. Traditional dollar savings accounts are not available to these populations even if they want them. The barriers are documentation requirements, minimum balance thresholds, physical bank branch proximity, and the bureaucratic complexity of formal banking relationships that many people in informal employment or rural areas simply cannot navigate.

A smartphone and a self-custody wallet have no minimum balance, no documentation requirements, no physical branch, and no application process. The stablecoin on-ramp through peer-to-peer markets, local exchanges, and increasingly through retail merchant networks has dramatically lower friction than any formal banking alternative. For populations that have historically been excluded from dollar-denominated savings by institutional barriers, stablecoins represent the first practical access they’ve had.

Limited cross-border payment options is the third driver, and it connects to the remittance economy that flows through the region at enormous scale. Latin America receives hundreds of billions in annual remittances from diaspora communities in the United States, Europe, and other regions. The traditional remittance infrastructure — Western Union, MoneyGram, bank wire transfers — extracts significant fees from those flows. USDT and USDC transfers through the altcoin ecosystem, as documented elsewhere, reduce those costs to fractions of a cent. Families receiving remittances who have shifted to stablecoin rails are not choosing an altcoin product for ideological reasons. They’re choosing it because more of the money sent actually arrives.

Why Bitcoin Lost the Competition It Didn’t Know It Was In

Bitcoin’s 18% share of Latin American altcoin purchases isn’t a failure of Bitcoin as a technology. It’s a market telling you something precise about what it needs that Bitcoin, by design, doesn’t provide.

Bitcoin’s volatility is a feature for investors with long time horizons and risk tolerance — the property that enables its asymmetric return potential is the same property that makes it unreliable as a short-term store of value or a medium of exchange in economies where people are living paycheck to paycheck. A person using altcoins to protect this month’s savings from currency depreciation cannot absorb a 20% Bitcoin correction. That correction doesn’t feel like a buying opportunity. It feels like losing the rent money.

Stablecoins eliminate that risk entirely. They don’t offer Bitcoin’s upside. They don’t need to. The populations driving Latin American stablecoin adoption aren’t optimizing for upside — they’re optimizing for preservation. Dollar stability at zero volatility is worth more to them than asymmetric return potential they can’t afford to wait for.

This distinction is fundamental to understanding how altcoin adoption in emerging markets differs from adoption in developed economies — and why applying a Western investment framework to interpret Latin American altcoin behavior consistently produces the wrong conclusions. When financial media notes that Bitcoin is lagging stablecoins in Latin American purchases and frames it as a Bitcoin adoption problem, it’s misreading the data. Bitcoin isn’t losing a competition with stablecoins. It’s operating in a different market segment, serving a different need, for a different population.

The USDT vs USDC Dynamic Within the Stablecoin Category

Within the 40% stablecoin share, the split between USDT and USDC reflects geographic and demographic patterns that the aggregate number obscures.

USDT’s dominance in peer-to-peer markets and informal economies across the region reflects its first-mover advantage and its penetration into the specific corridors — Venezuela, Argentina, parts of Brazil and Colombia — where the most acute currency crises have driven adoption. In these markets, USDT is effectively a vernacular currency. Merchants price goods in it. Workers negotiate salaries in it. Savings are denominated in it. It functions less like an altcoin and more like a local dollar economy that operates outside the formal financial system.

USDC’s presence is stronger in more formal contexts — regulated exchange platforms, business-to-business settlement, and corridors where compliance requirements favor a more transparently regulated issuer. As Latin American regulatory frameworks around altcoins develop and more formal businesses integrate stablecoin settlement, USDC’s share is likely to grow — not by displacing USDT in the informal economy, but by capturing the formal economy adoption that USDT’s regulatory posture makes harder to access in certain jurisdictions.

What This Means for the Global Altcoin Adoption Narrative

Latin America’s stablecoin preference data is a corrective to the dominant altcoin adoption narrative in two important ways.

First, it demonstrates that altcoin adoption at scale is not primarily driven by investment motivation. The populations generating Latin America’s altcoin volume aren’t looking for returns. They’re looking for stability, access, and utility. That’s a fundamentally different user base than the one that dominates Western altcoin discourse — and serving it requires fundamentally different products, interfaces, and infrastructure than the investment-oriented altcoin ecosystem has historically prioritized.

Second, it confirms that the stablecoin market’s trajectory toward Standard Chartered’s $2 trillion 2028 forecast isn’t dependent on speculative enthusiasm. It’s powered by structural demand from populations with genuine financial needs that stablecoins are uniquely positioned to address. That demand doesn’t evaporate in a bear market. It doesn’t correlate with Bitcoin’s price cycles. It’s driven by inflation rates, exchange rate policies, and banking access gaps that will persist regardless of what happens in the altcoin markets.

A region of 650 million people has voted with its purchasing behavior for what it needs from the altcoin ecosystem. The vote isn’t for Bitcoin’s volatility upside. It’s for dollar stability, instant transfer, and financial access without institutional gatekeeping. The altcoin ecosystem that serves that need — and builds the infrastructure to serve it better — has found a market that no bear cycle can take away.

Latin America stablecoin adoption 2025, USDT USDC Latin America purchases, stablecoins vs Bitcoin Latin America, Latin American altcoin market 2025, stablecoin inflation hedge emerging markets, USDT adoption Argentina Venezuela, Latin America crypto banking access, stablecoin 40% Latin America altcoin, Bitcoin 18% Latin America crypto, stablecoin dollarization emerging markets

Leave a Reply