Numbers like 420% growth in a single year tend to get dismissed as altcoin hype — the kind of figure that shows up in bull market marketing decks and disappears when the cycle turns. The tokenized real-world asset market’s surge past $30 billion deserves a different reading. Because unlike most altcoin growth narratives, this one isn’t driven by speculation, retail momentum, or the kind of reflexive price action that inflates and deflates with market sentiment. It’s driven by institutional capital moving into on-chain infrastructure for assets that existed long before blockchain did — and that will continue existing regardless of what Bitcoin’s price does on any given Tuesday.

The RWA market isn’t a crypto story wearing a finance costume. It’s a finance story that has decided blockchain infrastructure is the best available technology for solving problems that traditional financial plumbing has been failing to solve for decades.

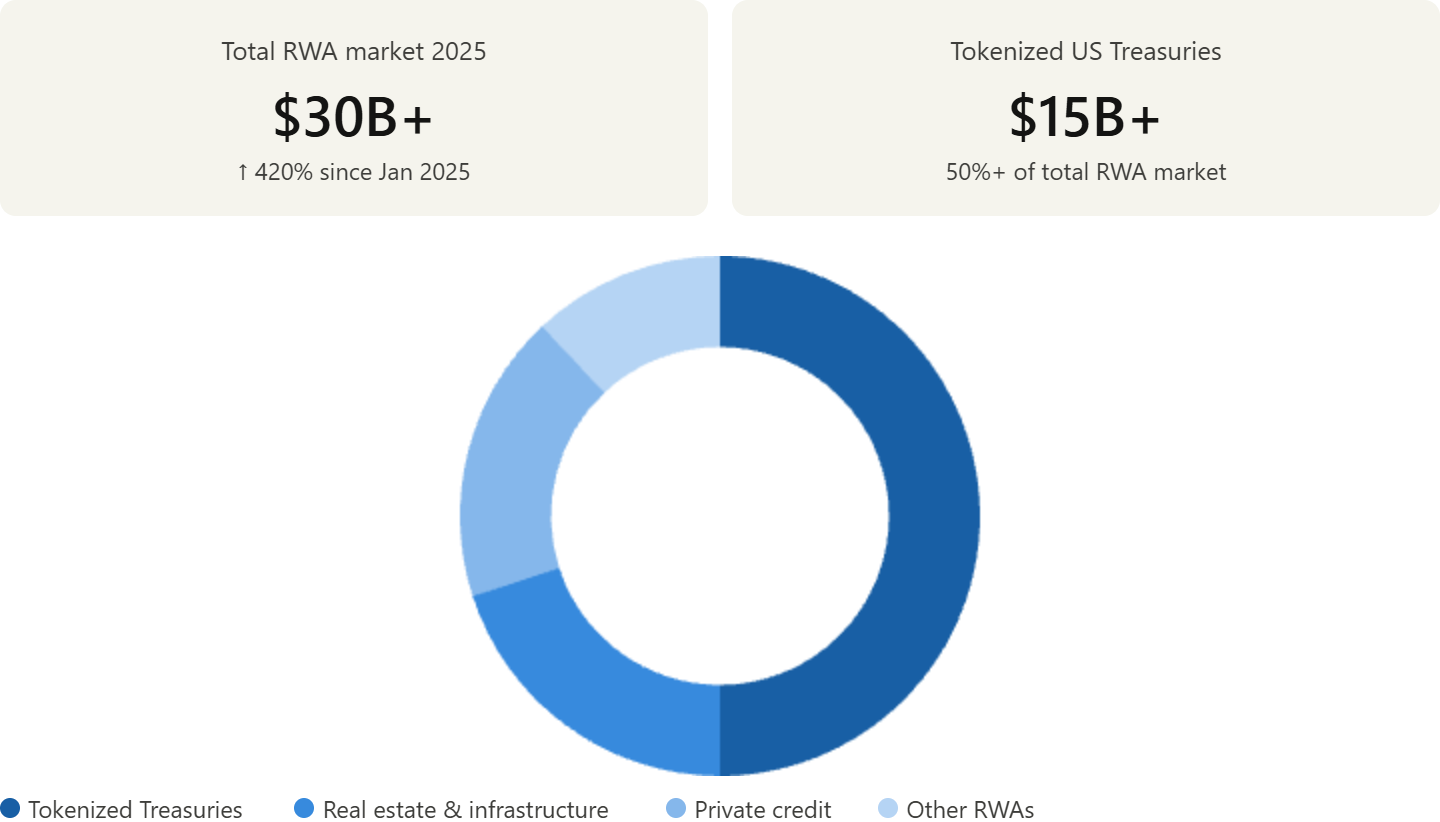

$30 Billion and the Asset That Got It There

The headline number — $30 billion in tokenized real-world assets, up more than 420% since January 2025 — is remarkable in its scale and its speed. But the composition of that number is where the real story lives. The single largest contributor to that growth was tokenized US Treasury bonds, which crossed $15 billion in on-chain volume. That’s more than half the total RWA market, sitting in a single asset class that most people would consider the least exotic financial instrument imaginable.

US Treasury bonds. The bedrock of traditional conservative investment. The asset that pension funds, sovereign wealth funds, and money market managers hold as the safest, most liquid, most boring store of value in global finance. That asset is now the dominant growth driver in what is nominally an altcoin ecosystem development story.

The reason is both simple and structurally significant. Tokenized Treasuries solve a specific and expensive problem that DeFi protocols have been grappling with since the beginning: the opportunity cost of holding capital in stablecoins waiting to be deployed. A dollar sitting in USDC earns nothing. A dollar sitting in a tokenized Treasury earning 4-5% yield while remaining on-chain, transferable, and usable as collateral in DeFi protocols — that’s a fundamentally different instrument. It’s yield-bearing liquidity. It’s the bridge between the safety of traditional finance and the composability of the altcoin ecosystem, and institutional capital has moved into it at a pace that reflects how long the market has been waiting for exactly that bridge to exist.

The players who have built the dominant tokenized Treasury products — BlackRock’s BUIDL fund, Franklin Templeton’s BENJI, Ondo Finance’s OUSG — aren’t altcoin-native projects experimenting with novel financial instruments. They’re asset managers with trillions under management who have concluded that on-chain distribution of traditional fixed-income products is superior infrastructure to what they’ve been using. When BlackRock builds a tokenized money market fund on Ethereum, it isn’t making a statement about altcoins. It’s making a statement about settlement efficiency, 24/7 transferability, and the composability advantages of on-chain assets over legacy clearing infrastructure.

Why Tokenized Treasuries Unlocked Everything Else

The Treasury bond story is more than just one asset class having a good year. It’s the proof of concept that unlocked institutional confidence in the broader RWA category — and understanding why requires looking at what tokenized Treasuries demonstrated that previous RWA attempts hadn’t.

Earlier tokenization efforts — real estate, art, commodities — faced a consistent set of problems: illiquid underlying assets, complex legal structures for fractional ownership, uncertain regulatory treatment, and limited secondary market infrastructure. The pitch was compelling conceptually but delivered a product that was harder to buy, harder to sell, and harder to hold than the non-tokenized version of the same asset.

Tokenized Treasuries inverted every one of those problems. The underlying asset is the most liquid, most regulated, most institutionally familiar instrument in global finance. The legal structure for Treasury ownership is completely settled. The regulatory treatment is clear. The yield is real, immediate, and competitive. And the on-chain format delivers specific advantages — instant settlement, programmable composability with DeFi protocols, 24/7 transferability — that the traditional format cannot replicate.

The result was an RWA product that was genuinely better than its off-chain equivalent for a specific set of institutional use cases. That’s a different value proposition than “this is a blockchain version of something you already have” — it’s “this is a version of something you already have that does things the original can’t.” Institutional capital moved accordingly.

And as it moved, it proved something to the institutions still watching from the sidelines: the regulatory, legal, and operational infrastructure for holding significant value in tokenized assets works. That proof of concept is now accelerating interest in the next categories.

Tokenized Stocks and Funds — The Next Frontier

Analysts pointing to tokenized stocks and funds as the next growth driver are identifying an opportunity that’s structurally similar to the Treasury bond opportunity but an order of magnitude larger in addressable market.

Global equity markets represent tens of trillions in market capitalization. Mutual funds and ETFs manage additional tens of trillions. The friction embedded in traditional equity market infrastructure — T+1 or T+2 settlement delays, market hours limitations, minimum investment thresholds that exclude smaller investors, cross-border ownership complexity — is well-documented and widely criticized. Tokenization of equity assets addresses all of it simultaneously: instant settlement, continuous markets, fractional ownership enabling any investment size, and cross-border transferability without the correspondent bank chains that make international equity ownership administratively complex.

The regulatory pathway for tokenized securities in major jurisdictions is more complex than for Treasury bonds — equities carry different disclosure requirements, shareholder rights considerations, and market manipulation concerns than fixed-income instruments. But regulatory frameworks are developing. The SEC has been engaging more substantively with tokenized securities questions. European markets have sandbox frameworks for digital asset securities. Singapore and Hong Kong have been among the most proactive in creating workable regulatory environments for tokenized equity instruments.

The institutional appetite is clearly there. The infrastructure — smart contract platforms capable of handling the compliance logic of regulated securities, custody solutions that institutional asset managers are comfortable with, secondary market liquidity for tokenized equity positions — is maturing rapidly. The combination of demonstrated Treasury tokenization success and improving regulatory clarity creates conditions for equity tokenization to follow a similar adoption curve, potentially faster given the proof of concept already established.

The Altcoin Ecosystem’s Quiet Infrastructure Revolution

The RWA market’s 420% growth in 2025 is happening largely below the radar of the altcoin community’s typical attention metrics. It doesn’t show up in token price movements. It doesn’t generate the engagement that a new Layer 1 launch or a DeFi protocol’s yield numbers produce. The people moving capital into tokenized Treasuries aren’t posting about it on altcoin Twitter.

But it’s arguably the most significant development in the altcoin ecosystem’s maturation as financial infrastructure — more significant, in terms of long-term structural impact, than most of what does capture community attention. Every dollar of institutional capital that moves into on-chain tokenized assets is a dollar that has crossed the barrier between traditional finance and blockchain infrastructure and decided to stay. It’s capital that has validated, with real money and real fiduciary responsibility, that on-chain settlement works for serious institutional use cases.

That validation has compounding effects. Institutions that hold tokenized Treasuries build operational familiarity with on-chain asset management. Risk committees that approved Treasury tokenization have established frameworks that make subsequent approvals — for tokenized equities, tokenized private credit, tokenized real estate — easier to navigate. Custody providers, legal teams, and compliance functions that have processed tokenized Treasury positions have built the institutional muscle memory for handling the next category.

The $30 billion RWA market isn’t a destination. It’s an early data point on an adoption curve that the Treasury bond success has just made significantly steeper. The altcoin ecosystem built the infrastructure. Traditional finance is now loading it with the assets that actually move global capital.

RWA market 420% growth 2025, tokenized real world assets $30 billion, tokenized US Treasury bonds $15 billion, RWA market growth drivers, tokenized stocks funds next stage, real world asset tokenization 2025, BlackRock BUIDL tokenized Treasury, altcoin RWA market expansion, tokenized assets institutional adoption, RWA DeFi composability yield

Leave a Reply