Sixty percent. That’s how much altcoin adoption exploded across Latin America heading into 2025 — and the numbers behind that figure tell a story the traditional financial system really doesn’t want you reading.

For years, the dominant narrative around altcoins in the region was straightforward: people held Bitcoin and other assets as a hedge against runaway inflation. Argentina. Venezuela. Brazil. Countries where your savings could lose double-digit purchasing power in a single year made it obvious why people looked for alternatives. That narrative wasn’t wrong — it was just incomplete. Because what’s happening now goes far beyond protecting savings. It’s about replacing the pipes that money flows through entirely.

$730 Billion and Counting

The headline number from 2025 is staggering: stablecoin transfers across Latin America hit $730 billion, making them the dominant form of altcoin movement in the region by a wide margin. This isn’t speculative volume driven by traders flipping positions — this is utility. Real people. Real businesses. Real transactions that used to flow through wire transfers, correspondent banking networks, and currency exchange desks that quietly took a slice every single time.

Stablecoins — dollar-pegged assets like USDC and USDT that sit within the broader altcoin ecosystem — have essentially hacked the international payments layer. And the numbers explaining why are almost comically one-sided.

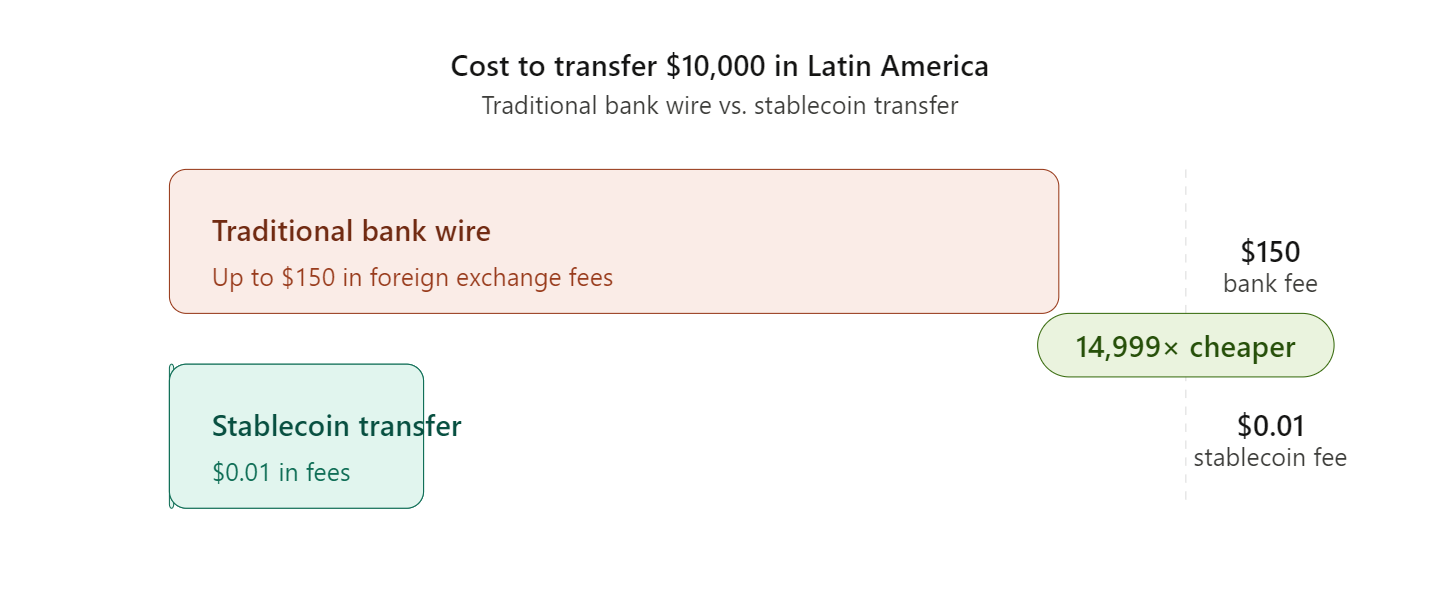

The Fee Gap That Changes Everything

Let’s visualize just how dramatic the cost difference really is:

According to data from Polygon, sending $10,000 across borders in the region can cost up to $150 in foreign exchange fees through traditional banking channels. The same transfer using stablecoins? $0.01. Not one dollar. One cent. That’s not a marginal efficiency gain — that’s a structural demolition of the middleman.

For small business owners importing goods, freelancers getting paid by international clients, or families receiving remittances, those fees aren’t an abstraction. They compound. They’re money that doesn’t reach the people it’s meant for. The altcoin ecosystem, specifically through dollar-pegged stablecoins, has made that friction essentially disappear.

Beyond Inflation — The Trade Finance Angle

The original use case for altcoins in Latin America was defensive: don’t let your savings evaporate. That’s still relevant in several economies across the region. But 2025 revealed a far more sophisticated adoption pattern — one that’s offensive, not defensive.

Businesses across Latin America are now using stablecoins to access global trade finance. This is a significant expansion of how the altcoin ecosystem is being applied. Rather than simply storing value away from local currency risk, companies are actively denominating trade deals, invoicing international partners, and settling cross-border commercial transactions on-chain.

This shift has implications that go well beyond what most Western observers typically associate with crypto adoption. It means altcoins are becoming embedded in the supply chain fabric of a region home to over 650 million people. That’s not speculative enthusiasm — that’s infrastructure.

Why This Matters for the Broader Altcoin Narrative

The Latin American stablecoin surge is a case study the entire altcoin community should be studying closely. It proves a few things that often get lost in market cycle discussions.

First, adoption is driven by real economic pain, not hype. The 60% growth in altcoin usage didn’t happen because of a bull market pump. It happened because people needed a tool that worked better than what they had. When something solves a genuine problem this efficiently, adoption accelerates regardless of token prices.

Second, stablecoins are the entry point. While the broader altcoin ecosystem offers everything from DeFi yields to NFT marketplaces, the gateway for mass regional adoption has been boring, functional, dollar-pegged utility. People aren’t arriving in the altcoin space chasing 100x returns — they’re arriving because they want to send money without losing 1.5% to a bank.

Third, and perhaps most importantly, this signals how the traditional banking system is losing relevance in real-time in large parts of the world. The $730 billion in stablecoin transfers across Latin America isn’t volume that flowed alongside traditional finance — much of it replaced it.

The Numbers Are Just Getting Started

A 60% adoption jump is impressive for any technology sector. For altcoins in a region that’s historically been underserved by global financial infrastructure, it suggests the trajectory isn’t plateauing — it’s accelerating.

The conversion is already happening in the infrastructure layer. Businesses that have switched to stablecoin-settled invoices won’t revert to paying $150 per transfer. Freelancers receiving USDC payments won’t go back to waiting 3–5 business days and losing a percentage to exchange desks. Once the efficiency advantage is experienced firsthand, the old way simply becomes unacceptable.

Latin America in 2025 isn’t just a regional success story for the altcoin ecosystem. It’s the clearest real-world proof yet that the technology works, that it scales, and that when traditional financial systems fail people badly enough, the migration to altcoin rails doesn’t need evangelism — it needs only an internet connection.

Leave a Reply