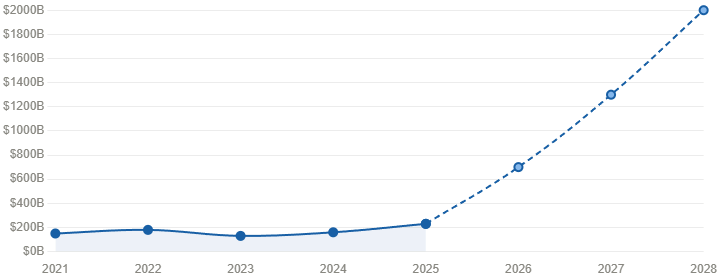

When Standard Chartered first put a $2 trillion figure on the stablecoin market by 2028, the reaction from traditional finance was predictable: polite skepticism wrapped in carefully worded caveats. The bank hasn’t blinked. Its forecast stands — and the data it’s now publishing to support that conviction is arguably more interesting than the headline number itself.

Stablecoin velocity has doubled in two years. Tokens are now changing hands an average of six times per month. That single metric reframes the entire stablecoin narrative in ways the altcoin community should be paying close attention to.

From Store of Value to High-Frequency Settlement Layer

Velocity is the metric that separates a savings instrument from a payments infrastructure. Gold has near-zero velocity. Cash in a mattress has zero velocity. A currency actively circulating through an economy has high velocity — it’s being used, not just held.

The fact that stablecoin velocity has doubled over 24 months tells you something fundamental has shifted in how these assets are being deployed. This isn’t a cohort of altcoin holders sitting on dollar-pegged tokens waiting for market conditions to improve. This is active, repeated, high-frequency transactional use — the kind that looks less like speculative positioning and more like, well, money.

Six transactions per token per month isn’t just an improvement on previous figures. It’s a credible challenge to the velocity profiles of traditional payment instruments in certain corridors. And it’s happening without the backing of a central bank, a national mandate, or decades of payment infrastructure buildout.

The trajectory toward $2 trillion isn’t a straight line extrapolation of current market cap. It’s a bet on behavioral adoption at scale — and the velocity doubling is precisely the kind of leading indicator that makes that bet look increasingly rational.

Two Stablecoins, Two Completely Different Jobs

One of the most analytically useful things Standard Chartered’s reporting does is separate USDC and USDT into distinct functional categories. Most coverage of the stablecoin market treats them as interchangeable — both dollar-pegged, both widely held, both part of the same asset class. The reality on the ground is considerably more nuanced.

USDC has become the dominant stablecoin in payment system integration. Its velocity story is tied directly to its role as a settlement layer inside emerging payment infrastructure — the kind that’s replacing traditional banking rails in cross-border commerce, freelancer payouts, B2B invoicing, and corporate treasury operations. Every time a payment platform routes a transaction through USDC instead of a wire transfer, that contributes to velocity. Every time a company settles a cross-border invoice on-chain, velocity ticks up. USDC’s rise is fundamentally a payments infrastructure story, and it’s accelerating because the efficiency gap between stablecoin settlement and TradFi alternatives is simply too large to ignore once you’ve experienced it firsthand.

USDT tells a different story entirely. In emerging markets across Southeast Asia, sub-Saharan Africa, Latin America, and Eastern Europe, Tether functions less like a transactional currency and more like a digital savings account denominated in dollars. Populations with limited access to USD-denominated bank accounts, or living in economies where local currency depreciation is a constant background anxiety, have adopted USDT as a reliable store of value. It sits in wallets the way physical dollars used to sit in mattresses — a hedge against local monetary instability that doesn’t require a US bank account or a relationship with an international broker.

These aren’t competing use cases. They’re complementary ones, and together they explain why the stablecoin market is exhibiting both high velocity and strong market cap growth simultaneously — a combination that’s unusual in traditional monetary economics and reflects the genuinely dual nature of what stablecoins have become.

What $2 Trillion Actually Requires

Standard Chartered’s forecast isn’t contingent on altcoin markets entering a bull cycle or Bitcoin hitting some new all-time high. It’s contingent on adoption curves that are already visible and already accelerating. But getting from current market size to $2 trillion by 2028 requires a few things to go right that aren’t guaranteed.

Regulatory clarity is the most obvious prerequisite. The US stablecoin legislation that’s been in various states of congressional negotiation has significant implications for whether USDC can continue its payment infrastructure expansion into regulated financial environments. If clear rules emerge that allow banks and payment processors to integrate stablecoins without compliance ambiguity, the adoption flywheel accelerates dramatically. If regulatory gridlock continues, growth will be slower and more fragmented — real, but constrained by institutional reluctance.

The second prerequisite is continued infrastructure buildout. The altcoin ecosystem’s underlying payment rails — the Layer 2 networks, cross-chain bridges, and on/off ramp infrastructure that make stablecoins practically usable for non-technical users — are still maturing. Velocity doubling is impressive. But six transactions per month per token is still modest compared to what mature payment networks handle. Getting to $2 trillion means bringing in users for whom “download a wallet and buy crypto” is still a significant friction point.

Why TradFi Should Be More Concerned Than It Appears

The framing of stablecoins as a complement to traditional finance — rather than a replacement — has been the diplomatic position that most altcoin-adjacent institutions have adopted when speaking to regulators and banking partners. Standard Chartered, as a major international bank, is no exception to that diplomatic instinct.

But the underlying dynamic that its own data describes is less complementary and more substitutional than the language suggests. USDC adoption in payment systems is explicitly described as replacing TradFi rails, not supplementing them. Businesses choosing stablecoin settlement aren’t running it alongside their existing bank transfers for redundancy — they’re switching because the cost and speed differential is decisive.

When a $2 trillion asset class with doubling velocity is described by one of the world’s largest banks as replacing traditional finance infrastructure, the polite word for what’s happening is disruption. The less polite word is displacement. Either way, Standard Chartered maintaining its $2 trillion forecast isn’t just a bullish call on an altcoin-adjacent asset class. It’s a bank publicly acknowledging that a significant portion of what banks have traditionally done — moving money across borders efficiently and cheaply — is being done better by the ecosystem it’s also choosing to analyze and track.

That’s a remarkable position for a 160-year-old institution to find itself in. And it tells you more about where stablecoins are headed than any price chart could.

Leave a Reply